The real estate sector is one of the most globally recognized and vital contributors to economic development. In India, it is projected

to contribute 13% to the country’s GDP by 2025

, driven by rapid urbanization and strong growth across residential, commercial,

retail and hospitality real estate - all of which are laying the foundation for India’s next phase of infrastructure and economic

expansion.

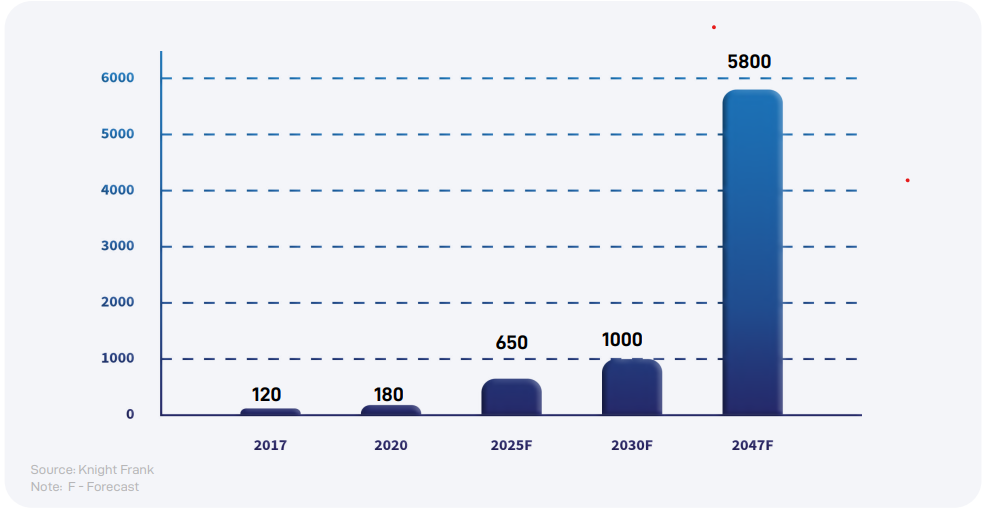

The market size of Indian real estate is projected to experience a substantial increase, potentially reaching a value of US$ 5-7 trillion

by the year 2047, with the possibility of surpassing US$ 10 trillion

Exhibit 1: India’s real estate market size (US$ billion)

This structural shift is further amplified by the rise of wealthy individuals that is increasingly approaching real estate with a more strategic and diversified lens. In India, the number of wealthy individuals is projected to grow by 50.1% between 2023 and 2028, making it a key market for alternative investment strategies. Notably, as much as 32% of their wealth is currently allocated to residential real estate, highlighting a strong preference for this long-term asset.

However, in a landscape marked by heightened volatility across global markets, traditional real estate investment-once considered a cornerstone of wealth preservation-is being increasingly re-evaluated.

While real estate remains a powerful asset class, direct ownership presents structural challenges, including concentration risk, management complexity and regulatory hurdles. In this context, Real Estate Alternative Investment Funds (AIFs) are emerging as an attractive vehicle—offering investors access to high-growth opportunities with built-in diversification, institutional oversight, and regulatory guardrails

As India’s real estate sector matures and scales, real estate AIFs are uniquely positioned to capitalise on this inflow of capital and growing investor interest. These funds not only unlock access to India’s property market but also solve the inefficiencies of direct investing-making them a preferred vehicle for wealthy investors and institutions seeking risk-managed exposure to income-generating real estate.

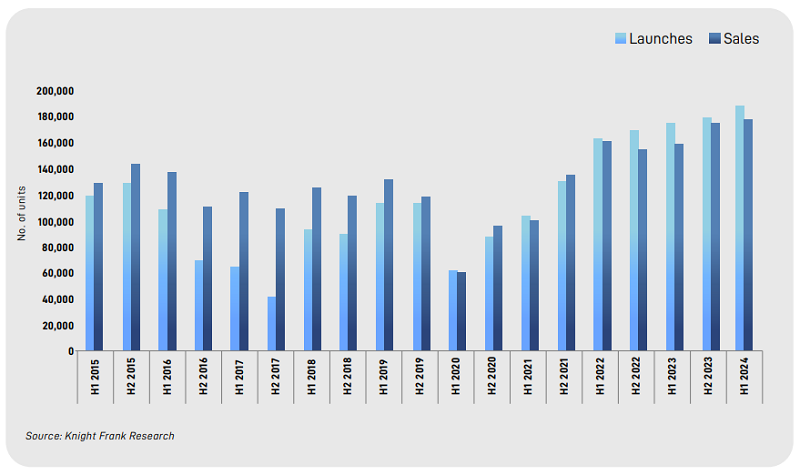

India’s growing real estate market is increasingly integrated with global investment trends due to its rapid economic growth, urbanization, digital adoption, innovative technological solutions and evolving investment opportunities. The Indian real estate market is projected to catapult from $350 billion in 2023 to a staggering $1 trillion by 2030 . Several key segments within the Indian real estate market are capturing the attention of investors, particularly through AIFs. The residential sector, with its booming demand in major cities like Delhi, Mumbai, Pune, Hyderabad and Bengaluru, continues to attract significant capital. Since the pandemic, the real estate industry has rebounded across all segments, with the residential market witnessing the fastest and most significant resurgence.

Exhibit 2: Launches and sales trend of residential real estate in India

Concentration Risk: Individual investors often allocate substantial capital into a few properties or a few assets. This lack of spread increases vulnerability to market-specific cycles—be it a downturn in commercial real estate or stagnation in a residential locality, Or any other scheme may have a limited number of investments and, as a consequence, the aggregate returns realized by the contributors may be adversely affected by the unfavorable performance of a small number of such investments. Since many of the investments may involve a high degree of risk, poor performance by a few of the investments could significantly affect the total returns to the contributors

Lack of Professional Management: Individual investors often lack the professional management expertise needed to optimise real estate portfolios. This includes understanding zoning regulations, tenant management, risk assessment, and leveraging financial instruments to maximise returns. Unlike mutual funds or equities, individual property investors lack access to institutional-grade management. This results in rental yields, tenant risk, and underperformance compared to managed portfolios.

Regulatory and taxation hurdles: Owning and managing property—especially across states or countries—brings compliance risks. Multiple state-level taxes, GST on commercial leases, and capital gains complexities increase friction.

High entry barriers and uncertain exits: Direct real estate investments often require substantial capital outlay - especially for premium, well-located assets - and exits are heavily dependent on market conditions, which can lead to delays or discounted sales during low-demand periods

Real estate AIFs, particularly Category II AIFs under SEBI regulations, address many of the above issues by pooling investor capital into a professionally managed and diversified vehicle. Here’s how they contribute to diversification:

Asset class diversification:

The regular real estate investing in India-especially among individual HNIs-tends to

be heavily skewed toward residential assets. AIFs invest across real estate verticals -residential, commercial office, logistics parks, warehousing, data centres, and even co-living/student housing. This multi-segment approach reduces reliance on any single asset class.

While traditional investors tend to “go where they live,” AIFs invest where the economy is growing.

Geographic diversification: The diversification across geographies further strengthens the proposition. Real Estate AIFs often invest across major metro cities—such as Mumbai, Delhi NCR, and Bengaluru—as well as in emerging urban hubs like Pune, Ahmedabad, and Kolkata. Home sales in Mumbai stand at a 13 year high with 47,259 units sold in H1 2024 constituting a healthy 16% YoY growth5 , while Hyderabad scaled a new all-time high in H1 2024 with 18,573 units sold during the period. Such a strategy not only spreads risk but also taps into high-growth pockets driven by urbanisation and infrastructure development.

Exhibit 2: Launches and sales of residential real estate in India (No. of units)

Risk management: The diversification is coupled with sophisticated risk management strategies, enabling these funds to navigate various market cycles effectively. Professional fund managers continuously monitor and rebalance portfolios in response to market shifts, policy changes, and economic indicators. This dynamic approach helps in mitigating downside risk while seeking alpha returns.

Easier and more secure liquidation: Unlike direct property sales that rely on demand-supply for a specific asset, AIFs offer structured project-level exits, often with secured exposure - enhancing liquidity and providing greater certainty in the realisation of invested capital.

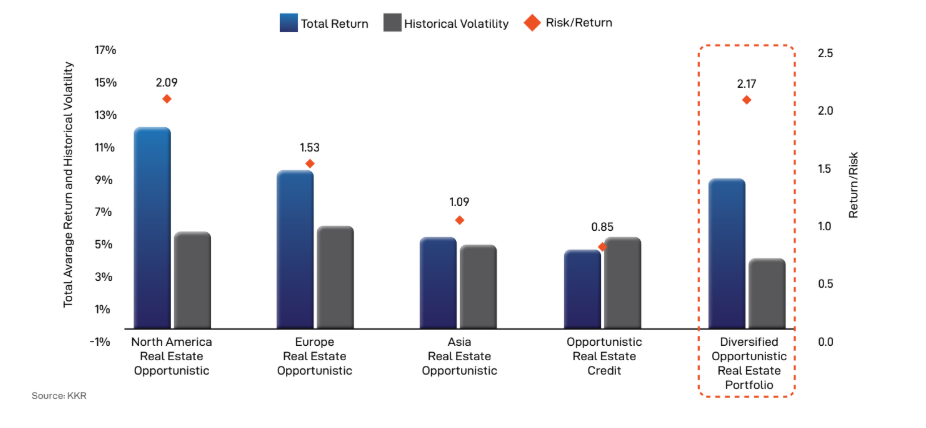

Exhibit 3: Performance over 10-Year Period8 ( Q2’2013 to Q2’2023)

A study by KKR on opportunistic real estate indicates that Over 2013–2023, diversified opportunistic real estate portfolios delivered a superior return/risk ratio of 2.17 vs. 2.09 (North America), 1.53 (Europe), 1.09 (Asia), and 0.85 (real estate credit).

This reinforces the compelling case for strategic diversification across geographies, asset classes, and investment strategies with- in real estate AIFs. As real estate markets across the globe exhibit varying cycles of growth, yield compression, and regulatory shifts, Indian HNIs and institutions are increasingly recognizing the need to look beyond domestic opportunities.

In essence, the future of real estate investing lies not in concentration, but in thoughtful allocation—across debt and equity, across borders, and across real estate use cases. Real estate AIFs offer the structural flexibility and professional management to imple- ment this at scale.

7th Floor, B 707, Kohinoor Square, N C. Kelkar Rd, opp. Shiv Sena Bhavan, Dadar-W, Mumbai, Maharashtra. 400028

© 2025 Infradawn Capital. All rights reserved.

Sitemap